Telsa sales are falling. Toyota Prius went out of the running a decade ago. iPhone stare at a similar fate. Once competitors catch up, improve the formula, reduce manufacturing costs, and flood the market with alternatives, the innovation premium collapses

For more than a century of industrial history, one pattern has repeated with astonishing consistency: the first mover—the company that introduces a transformative, category-defining innovation—enjoys extraordinary pricing power and prestige. Consumers are willing to pay a premium not merely for utility, but for novelty, status, and technological superiority.

But that premium is fragile.

Once competitors catch up, improve the formula, reduce manufacturing costs, and flood the market with alternatives, the innovation premium collapses. The once-revolutionary product becomes ordinary. The pioneer loses ground and pricing power erodes rapidly.

Today, Tesla and Toyota hybrids are the most visible examples of this decline. Both companies reshaped global automotive technology—Tesla with electric vehicles and Toyota with hybrids. For years, they charged premium prices supported by innovation leadership, brand prestige, and limited competition.

That era is ending.

Tesla: The loss of a premium built on innovation

Only two years ago, Tesla could command luxury pricing even for relatively minimalist interiors and limited model options. Buyers paid because Tesla symbolized technological superiority, environmental leadership, and Silicon Valley futurism. Owning a Tesla meant owning the future.

Today, the narrative has changed dramatically.

Sales collapse across major markets

Tesla’s sales trajectory reflects a brand losing its premium:

- Europe: down 48.5% year-on-year in October

- China: down 35.8% in October, 8.4% year-to-date

- Global deliveries: expected to decline 7% this year after falling 1% in 2024

Meanwhile, the industry-wide EV market in Europe grew 26% in the same period. Tesla is shrinking in a growing market—a devastating sign of competitive displacement.

Competitors offering more for less

Tesla once dominated with unique features: long range batteries, fast charging, minimalist design, and over-the-air software updates. Today:

- Chinese brands such as BYD, Xiaomi, and Chery offer cheaper, better-equipped EVs

- European brands like Volkswagen have caught up in range and performance

- Over 150 EV models now compete in the UK alone

- At least 50 new EV models will enter Europe next year—none of them Teslas

BYD sold more than double Tesla’s European volumes in October. Volkswagen tripled Tesla’s EV sales in Europe this year, with VW’s EV sales rising 78.2% to 522,600 units.

The innovation gap has closed—but Tesla has not refreshed its lineup. The company still largely depends on two mass-market vehicles: the Model 3 and Model Y, both launched years ago.

Price cuts signal lost pricing power

Tesla has been forced to introduce stripped-down versions of the Model Y and Model 3, cutting prices by around $5,000. Price cuts in an inflationary environment are a clear indicator of collapsing premium positioning.

Toyota Hybrid: A former revolution now a commodity

Two decades ago, Toyota’s Prius was a technological marvel. It symbolized environmental consciousness and engineering innovation. Celebrities drove it. Governments subsidized it. Toyota charged premium prices because it had no real competition.

Today, hybrid technology is everywhere.

Nearly every major automaker now offers hybrid or plug-in hybrid models:

- Hyundai

- Kia

- Honda

- Ford

- Volkswagen

- Chinese manufacturers

- Luxury brands like Lexus, BMW, and Mercedes

The result:

- Toyota hybrid sales have fallen

- Hybrid pricing has collapsed

- The Prius has lost its status symbol appeal

What was once an innovation premium is now basic automotive engineering.

The broader pattern: Innovation premiums always decline

Tesla and Toyota are not isolated cases. Industrial history is full of examples where early innovators dominated temporarily, charged premium prices, and later lost that ability once the competition matured.

Below are several powerful parallels.

Smartphones: The iPhone premium erosion

When Apple introduced the iPhone in 2007, it enjoyed an innovation premium that allowed:

- high margins

- premium pricing

- cultural dominance

But today:

- Chinese brands like Xiaomi, Oppo, Vivo, and Huawei offer high-spec smartphones for a fraction of the price

- Foldable phones, AI camera systems, and extreme fast-charging innovations are coming from rivals—not Apple

- Apple’s sales growth has slowed sharply in several markets, especially China

The iPhone is now losing premium justification, relying more on brand loyalty than innovation.

Dyson: When engineering luxury becomes replicable

Dyson revolutionized:

- bagless vacuum cleaners

- bladeless fans

- premium hair dryers

Consumers paid eye-watering prices for products perceived as engineering masterpieces.

Today:

- Chinese and Korean brands produce similar products at one-third the price

- Technology has been reverse engineered

- Dyson’s growth has slowed

- Its pricing power has weakened

Innovation leadership declined, and so did the premium.

GoPro: From innovation icon to commodity

GoPro pioneered action cameras and charged premium prices. But once:

- smartphones improved video capabilities

- competitors like DJI entered with superior stabilization and features

- Chinese manufacturers flooded the market

GoPro lost its pricing power and saw sales and relevance plummet.

Netflix: The subscription innovation that became generic

Netflix invented:

- the dominant streaming subscription model

- binge-watching culture

It could once raise prices with little pushback.

Today:

- dozens of streaming competitors exist

- production costs have exploded

- consumers cancel quickly

- Netflix’s pricing power is limited

Streaming is now a commodity, and profitability is difficult.

Bose and noise-cancelling headphones

Bose once charged a massive premium for its industry-leading noise cancellation.

But:

- Sony

- Apple AirPods Max

- Sennheiser

- Chinese brands

now offer comparable or better performance, often cheaper. Bose no longer commands the same authority or pricing.

Nespresso and the capsule coffee premium collapse

Nespresso pioneered capsule coffee and charged luxury prices for:

- machines

- capsules

- exclusive flavors

But once patents expired:

- supermarket capsules flooded the market

- third-party machines emerged

- price competition exploded

Nespresso lost exclusivity—and pricing power.

The walkman and Sony’s lost dominance

Sony created:

- portable music

- compact disc players

- early digital audio

It dominated global electronics.

Then:

- Apple introduced the iPod

- Smartphones absorbed music functions

- Competitors matched features

Sony’s innovation premium evaporated, and it became a follower brand.

Why the innovation premium disappears

Several structural mechanisms drive this pattern:

1. Technological diffusion

Competitors learn, copy, reverse engineer, and improve innovations faster than ever.

2. Economies of scale

High-volume manufacturers—especially Chinese firms—can produce comparable technology at lower costs.

3. Consumer fatigue

Once innovation becomes familiar, consumers stop paying extra for it.

4. Market saturation

Early adopters pay premiums; mass-market buyers demand value.

5. Regulatory and incentive changes

Subsidies and tax credits that once supported premium pricing disappear.

Tesla’s recent U.S. sales spike vanished immediately after a tax credit expired—proof of weakened intrinsic demand.

Tesla’s additional challenges

Tesla faces problems beyond competition:

- Limited model lineup

- Aging designs

- Negative brand perception due to political controversies

- CEO distraction with robotics and social media

- Focus on robotaxis instead of new consumer models

Analysts note that Tesla appears unprepared for the next phase of the EV market.

The future: Autonomy or irrelevance?

Elon Musk increasingly emphasizes:

- self-driving

- robo-taxis

- humanoid robots

He hopes autonomy will recreate an innovation premium.

However:

- no new mass-market Tesla vehicle is confirmed

- regulatory barriers remain

- competitors are developing similar technologies

Tesla’s new CEO compensation package allows enormous payouts without requiring major sales growth, suggesting the company expects stagnation in vehicle sales.

Innovation buys time, not permanence

Tesla and Toyota transformed the automobile industry. Their innovations justified premiums for years. But innovation premiums are temporary.

History shows:

- innovation leadership erodes

- competition intensifies

- pricing power disappears

From iPhones to Dyson, from Bose to Netflix, from Nespresso to GoPro, the same story repeats.

Innovation is no longer enough.

To sustain premium pricing in the modern market, companies must:

- continuously innovate

- refresh product lines

- expand offerings

- invest in design and experience

- maintain strong branding

Tesla has not done this.

Toyota hybrids no longer feel special.

The innovation premium that once seemed unassailable has vanished, leaving both companies facing a future where their products are judged not as revolutionary, but simply as options in a crowded marketplace. And in that world, price—not innovation—becomes the deciding factor.

The sunset of the EV first-mover: Tesla’s price war

When Tesla first launched the Model S, it was not merely selling an electric car; it was selling a futuristic statement—a blend of high performance, minimalist design, and an unparalleled charging network. This combination justified a substantial premium, allowing the company to operate with industry-leading profit margins. Today, however, that era is over.

The core argument provided in the initial text—that “Tesla is no longer an innovation. Therefore, it cannot charge that premium it used to charge for being a first mover”—is powerfully supported by recent sales data, which highlights a sharp deceleration in growth and a necessary reliance on deep price cuts.

Definitive sales data: The 2024 deceleration For years, Tesla’s annual delivery numbers boasted triple-digit, then strong double-digit, growth. The decline in its market standing began to crystallize in 2024 and early 2025.

The 1.1% drop in global deliveries in 2024 marked Tesla’s first annual decline in sales since 2011, according to analytics firms.2 This slowdown accelerated dramatically in the first quarter of 2025, with sales dropping by 13% year-over-year.3

The primary cause of this deceleration is not simply waning interest, but market saturation and hyper-competition, particularly in key global markets:

- Europe: Tesla’s sales plummeted by 48.5% in October 2024 across Europe year-over-year. This decline is severe, especially compared to the overall European EV market, which grew by 26% in the same period. The market has been flooded with competitive offerings, with the United Kingdom alone offering over 150 electric models. In a stark example of fading dominance, Germany’s Volkswagen (VW) posted an EV sales rise of 78.2% through September 2024, far outpacing Tesla in the region.

- China: Once a strong growth engine, Tesla’s deliveries in China fell by 35.8% in October 2024 to a three-year low. Chinese champions like BYD—which recently surpassed Tesla to become the world’s leading seller of battery electric vehicles (BEVs) in the second half of 2023—and newcomers such as Xiaomi are offering models that are often cheaper and boast faster innovation cycles.4

Insights from consulting and multilateral organizations

The erosion of Tesla’s premium is a textbook case of competitive pressure forcing price reduction to maintain volume. Analysts polled by FactSet estimated Tesla’s average sales price fell to just over $41,000 in Q4 2024, its lowest in at least four years.

According to the International Energy Agency (IEA), in its Global EV Outlook 2024 analysis, fiercer competition and price wars among OEMs (Original Equipment Manufacturers) have become the defining characteristics of the EV market.5 The report notes that in China, the price of compact electric cars and SUVs dropped by up to 10% in 2023 relative to 2022.6 Tesla’s response—aggressive price cuts—is a direct admission that the company can no longer sustain its high-margin pricing based on its brand alone; it must now compete on value and affordability.

A report from the consulting firm McKinsey & Company on the EV transition in Europe highlights that Chinese OEMs have demonstrated the ability to reduce time-to-market to less than two years, which is more than twice as fast as established European players.7 This compressed innovation cycle means any technological advantage held by a first-mover like Tesla is quickly neutralized, necessitating a focus on rapid, “design-to-value” production rather than relying on a historical premium.

The hybrid precedent: The case of the Toyota Prius

Long before Tesla redefined electric mobility, the Toyota Prius pioneered the mass-market hybrid vehicle in the late 1990s. The Prius, particularly its iconic second-generation model, was the ultimate eco-statement—a premium item that granted access to carpool lanes and boasted fuel economy that competitors couldn’t touch.

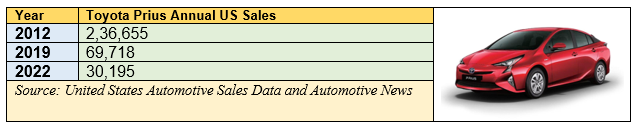

The Prius commanded a tangible premium. Initially introduced in the U.S. in 2000 with a published retail price of US$19,995, it was positioned above comparable conventional sedans like the Corolla. For over a decade, the Prius stood virtually unchallenged. Annual US sales peaked dramatically with the third generation (launched in 2009), reaching a high of 236,655 units sold in 2012, according to data published by the U.S. Bureau of Transportation Statistics and automotive analysts.

However, once the hybrid technology matured, the innovation premium vanished. Competitors—including Hyundai, Honda, Ford, and even Toyota’s own internal combustion engine (ICE) and conventional hybrid models (like the Camry Hybrid and RAV4 Hybrid)—diluted the Prius’s unique selling proposition. The necessity to purchase a dedicated, often polarizingly designed, hybrid car disappeared.

The nearly 87% collapse in US annual sales from its peak to its nadir in the early 2020s (before the recent 5th generation redesign brought a slight rebound) is a perfect statistical representation of innovation decay. Toyota itself moved toward a “multi-pathway approach,” integrating its hybrid technology seamlessly into its popular models, effectively cannibalizing the Prius’s unique market space. The first-mover advantage was exhausted by its own ubiquity.

The technological pioneer: The iPhone’s perpetual battle

The concept of innovation decay is not limited to automotive giants; it is perhaps most evident in consumer electronics, where product cycles are measured in months. The launch of the iPhone in 2007 created a new category and initially commanded an extraordinary premium for its touch interface, intuitive software, and integrated ecosystem. Apple’s initial pricing—starting at $499 or $599 with a two-year contract—was significantly higher than prevailing feature phones.

While Apple’s overall revenue has surged, its pricing power and unit volume stability have been constantly challenged, forcing the company to adapt through price segmentation.

iPhone sales and the strategy of value-tiering

Since Apple ceased reporting unit sales in 2019, revenue figures offer the best insight. In its fiscal year 2024, the iPhone generated $201.1 billion in revenue, representing approximately 51% of Apple’s total sales.8 Furthermore, global shipments in 2024 reached 232.1 million units. These massive figures, however, mask underlying competitive pressures.

Reports from the International Data Corporation (IDC) and other research firms consistently track how Apple has been forced to create a multi-tiered pricing structure (e.g., SE, standard, Pro, Pro Max) and use older models at lower price points to compete in budget-sensitive markets. The recent tepid demand reported for the relatively high-priced “iPhone Air,” according to IDC analysts, illustrates that even Apple cannot sell a premium product solely on innovation without delivering commensurate value and features.

Multilateral organizations observe this technological diffusion globally. Data from the OECD (Organisation for Economic Co-operation and Development) on technology diffusion and trade often shows that once a product category—like the smartphone—crosses a certain adoption threshold, competitive pressures from Asian manufacturers offering similar features at lower price points become immense, eroding the first-mover’s margins. Apple’s average selling price (ASP) remains high due to the success of its Pro Max variants, but its ability to sell entry-level phones at the historical first-generation premium has completely evaporated. The price of true innovation is now paid only for the ultra-premium, cutting-edge Pro models, while the entry-level models are competing on price and features available to nearly every other vendor.

Other casualties of innovation decay

The fate of Tesla, Prius, and the iPhone’s pricing model is simply a reflection of a pattern that defines the evolution of technology across industries:

- HDTVs: When High-Definition Televisions (HDTVs) first hit the market in the late 1990s, they cost thousands of dollars, far exceeding standard analog sets. A 42-inch plasma screen could easily cost over $10,000. Within a decade, driven by competition from manufacturers in East Asia, price-to-feature ratios plummeted. Today, a 4K 65-inch television costs a fraction of the original premium, thanks to panel standardization and efficiency.

- Digital Cameras: Early digital cameras, such as the 1997 Sony Mavica, were revolutionary but expensive and low-resolution. The premium on early megapixel counts quickly eroded as Japanese manufacturers ramped up production. The smartphone, itself a category defined by the iPhone, ultimately destroyed the standalone digital camera market by integrating the technology into a multi-function device, proving that continuous platform innovation is more valuable than single-product innovation.

- Fax Machines and VCRs: Once office staples and expensive consumer items, respectively, these products saw their premiums disappear entirely. The fax machine was replaced by email and digital document sharing, while the VCR and later the DVD player were swept aside by streaming technology. In both cases, the innovation premium collapsed to zero as superior, more affordable technologies emerged.

The Imperative for Continuous Renewal

The data from government agencies, consulting firms, and market sales—from the precipitous sales drop of the aging Tesla lineup in Europe to the historic decline of the Toyota Prius and the tiered pricing strategy of the iPhone—all confirm the same inescapable law of market economics: The innovation premium is a temporary rent paid by consumers for exclusivity, novelty, and superior functionality.

The speed of decay is determined by two factors: the replicability of the innovation and the competitive intensity of the market. The EV market, spurred by global policy goals and the entry of state-backed Chinese players, demonstrated both high replicability (VW caught up, BYD surpassed) and extreme intensity (price wars).

As noted by the European Parliamentary Research Service (EPRS) in its reports on EU-China EV competition, Europe’s own automotive sector is facing an existential crisis because the competitive advantage is shifting away from traditional manufacturing quality toward cost-efficiency and accelerated software/battery integration, areas where Chinese OEMs have achieved a lead.

Ultimately, the ability to charge some premium rests not on the memory of past breakthroughs, but on the delivery of present, non-replicable value. For companies like Tesla, the focus must shift from simply being a first-mover to becoming a fast-follower-of-self, leveraging continuous, vertically integrated innovation—robotics, AI, and next-generation platforms—to justify any remaining premium. Failure to do so condemns the pioneer to the inevitable fate of all initial disruptors: becoming the benchmark against which cheaper, faster, and equally functional competitors are measured.