Variations of cooperative housing have existed in India for decades, especially in cities like Mumbai and Ahmedabad. However, rising land prices and increased awareness of legal frameworks have made it more relevant today. With better access to legal advice, project management expertise, and digital tools, middle-class buyers are now better equipped to organize themselves into structured groups. Laziness prevents them from doing so

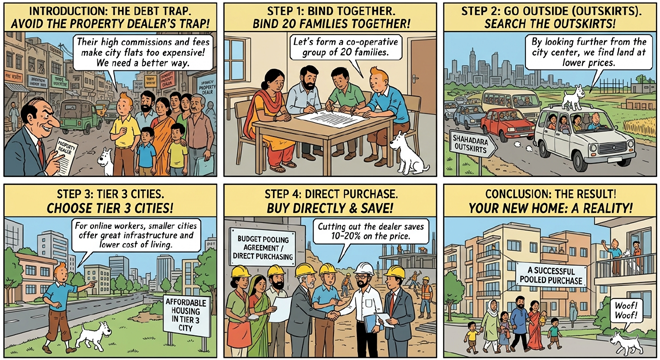

Buying a home in India is often described as a lifetime achievement, but it is equally a minefield of hidden costs, opaque practices, and inflated pricing. The so-called “property dealer trap” refers to a system where brokers and developers extract significant margins from buyers through commissions, price manipulation, and lack of transparency. In many urban and semi-urban markets, this can inflate property costs by anywhere between 15 percent and 40 percent. For middle-class families, this difference can determine whether homeownership is achievable or not.

One of the most effective ways to bypass this system is collective action, pooling resources with like-minded families to directly purchase land and construct apartments. This model flips the traditional hierarchy of real estate development. Instead of being passive buyers at the end of a long value chain, participants become active stakeholders who control costs, design, and execution. By eliminating intermediaries, they avoid broker commissions and developer profits, which are often the largest contributors to inflated prices.

This approach is not entirely new. Variations of cooperative housing have existed in India for decades, especially in cities like Mumbai and Ahmedabad. However, rising land prices and increased awareness of legal frameworks have made it more relevant today. With better access to legal advice, project management expertise, and digital tools, middle-class buyers are now better equipped to organize themselves into structured groups.

The appeal of this model goes beyond cost savings. It also ensures greater transparency. Buyers can directly monitor construction quality, select materials, and ensure compliance with regulations. This reduces the risk of common issues such as substandard construction, delayed possession, and disputes over promised amenities.

However, this model requires careful planning, trust among participants, and strict adherence to legal procedures. Without proper structure, it can lead to disputes and financial risks. Therefore, the first step is to formalize the group into a legal entity that can act as a single buyer and developer.

Forming a legal entity for collective ownership

The foundation of any successful group housing initiative is a robust legal structure. Informal arrangements are prone to misunderstandings and disputes, especially when large sums of money are involved. By forming a legal entity, the group ensures clarity in ownership, liability, and decision-making.

One of the most popular options is a cooperative housing society. This structure is particularly well-suited for residential projects because it aligns with the concept of shared ownership and collective management. Each member contributes funds and, in return, receives rights to a specific unit. The society as a whole owns the land and oversees construction.

Another option is forming a private limited company. In this model, each family becomes a shareholder, and the company owns the land. This structure offers flexibility and can be useful for larger projects, but it also comes with higher compliance requirements under corporate law.

A simpler alternative is a Body of Individuals, which can act as a single entity for purchasing land. While easier to set up, it may not offer the same level of legal protection as a cooperative society or company.

Regardless of the structure chosen, it is essential to define roles and responsibilities clearly. Who will manage finances? Who will liaise with contractors? How will disputes be resolved? These questions must be addressed through written agreements before any financial commitments are made.

Legal documentation is critical at this stage. Drafting a comprehensive agreement that outlines each member’s contribution, rights, and obligations can prevent conflicts later. It is advisable to engage a qualified lawyer who specializes in real estate to ensure that all legal requirements are met.

Land acquisition and due diligence essentials

Once the group is legally constituted, the next step is identifying and purchasing suitable land. This is arguably the most critical phase, as any mistake here can have long-term consequences. The goal is to deal directly with landowners, thereby avoiding brokers and reducing costs.

Due diligence is non-negotiable. The title of the land must be verified thoroughly, typically by examining a 30-year encumbrance certificate. This ensures that the land is free from legal disputes, mortgages, or claims. Any irregularity in the title can lead to prolonged litigation and financial loss.

Equally important is verifying land use zoning. The land must be classified as non-agricultural and approved for residential construction. Local building bye-laws and zoning regulations determine the type and scale of construction permitted. Ignoring these regulations can result in penalties or even demolition orders.

Registration of the sale deed is another crucial step. This must be done at the sub-registrar’s office, with all financial transactions properly documented. Each member’s contribution should be recorded clearly to avoid disputes over ownership.

Transparency in financial transactions is essential. All payments should be made through bank transfers, creating a clear paper trail. Cash transactions not only increase the risk of fraud but also complicate legal compliance.

Managing construction without a developer

After acquiring land, the group effectively becomes its own developer. This is where significant cost savings can be realized, but it also requires careful management. Instead of hiring a traditional developer, the group can engage professionals such as contractors and project management consultants.

Hiring a contractor on a per square foot basis is a common approach. This ensures that costs are directly linked to the size of the project, making budgeting more predictable. However, selecting a reliable contractor is crucial. References, past projects, and financial stability should be evaluated before finalizing the contract.

A project management consultant or architect plays a vital role in overseeing construction. They ensure that the contractor adheres to specifications, maintains quality, and completes work on schedule. This layer of oversight is essential to prevent cost overruns and substandard work.

A detailed development agreement should outline every aspect of the project, including the number of floors, unit sizes, and allocation of flats among members. This agreement acts as a blueprint for the entire project and must be drafted with precision.

Regular monitoring and communication are key to success. Periodic site visits, progress reports, and financial audits help keep the project on track. Transparency among members fosters trust and minimizes conflicts.

Financial planning and funding strategies

Financing a collective housing project requires disciplined planning. Unlike buying a ready-made flat, where payments are structured by the developer, group projects demand proactive financial management.

An escrow account is an effective tool for managing funds. All members deposit their contributions into a joint account, which is used exclusively for project expenses. Access to this account should be restricted to a few trusted individuals, with clear rules governing withdrawals.

Payments to contractors should be linked to construction milestones. For example, funds can be released after completion of the foundation, structure, and finishing stages. This ensures accountability and reduces the risk of incomplete work.

Home loans can also be availed for self-construction projects. Banks may require all co-owners to be co-applicants, and the approval process may be more stringent compared to standard home loans. However, the availability of financing makes the model accessible to a wider group of buyers.

Cost control is essential throughout the project. Bulk purchasing of materials, competitive bidding for contracts, and efficient project management can significantly reduce expenses. At the same time, quality should not be compromised in the pursuit of savings.

Ensuring legal compliance and regulatory adherence

Compliance with real estate regulations is critical to avoid legal complications. The Real Estate Regulatory Authority framework mandates registration for projects that exceed certain size or unit thresholds. Registering the project ensures transparency and protects the interests of buyers.

Issuing allotment letters to members is another important step. This formalizes the allocation of units and simplifies the process of ownership transfer once construction is complete.

Documentation must be meticulous. Every agreement, payment, and approval should be recorded and preserved. This not only ensures compliance but also provides a safeguard in case of disputes.

Penalties for delays and non-performance should be clearly defined in contracts. Even within a cooperative model, accountability is essential to ensure timely completion.

Exploring affordable housing on city outskirts

For those who prefer not to undertake construction, buying flats on the outskirts of cities offers another pathway to affordability. Peripheral areas typically have lower land costs, which translates into cheaper housing.

The key is to identify locations with growth potential. Areas that are 10 to 15 kilometers from city centers often offer a balance between affordability and accessibility. Infrastructure developments such as metro lines, highways, and industrial hubs can significantly enhance property values over time.

Cities like Ahmedabad, Pune, and Kolkata offer relatively affordable housing options compared to metropolitan giants like Mumbai and Delhi. Emerging suburbs in these cities provide opportunities for budget-conscious buyers.

However, affordability should not come at the cost of connectivity. Access to public transport, schools, hospitals, and employment centers is crucial for long-term livability.

Strategies for reducing costs when buying flats

Several strategies can help reduce the cost of purchasing flats. One of the most effective is buying under-construction properties, which are typically priced lower than ready-to-move units. However, this approach carries risks related to delays and project completion.

Resale properties offer another avenue for savings. These homes are often priced competitively and come with existing fittings, reducing additional expenses.

Group buying platforms enable multiple buyers to negotiate better deals with developers. By leveraging collective demand, buyers can secure discounts and favorable payment terms.

Choosing smaller configurations, such as one-bedroom units, can also make homeownership more accessible. These units are more common in affordable housing projects and require lower investment.

Leveraging government schemes and subsidies

Government initiatives play a significant role in promoting affordable housing. Schemes like the Pradhan Mantri Awas Yojana offer interest subsidies to eligible buyers, reducing the overall cost of home loans.

Eligibility criteria typically include income limits and first-time homebuyer status. Buyers should carefully review these requirements to determine their eligibility.

Investing in projects registered under the Real Estate Regulatory Authority provides an additional layer of security. These projects are subject to strict guidelines, reducing the risk of delays and fraud.

Negotiation tactics and due diligence

Negotiation is a critical skill in real estate transactions. Buyers should focus on the carpet area rather than the super built-up area to understand the actual usable space. Avoiding premium amenities can also reduce costs, as these features often increase both the purchase price and maintenance expenses.

Builders in suburban areas may offer flexible payment plans and discounts. Early-bird offers and festival schemes can provide additional savings.

Due diligence remains essential. Verifying the reputation of the builder, checking for hidden charges, and ensuring proper documentation can prevent costly mistakes.

Affordable cities and emerging opportunities

Several Indian cities offer affordable housing options with strong growth potential. Indore, Jaipur, Nagpur, and Lucknow are among the cities where property prices remain within reach for middle-class buyers. These cities combine infrastructure development with relatively low living costs.

Ahmedabad and Coimbatore stand out for their balanced growth and quality of life. Bhopal and Kochi offer affordability along with environmental and lifestyle advantages. Smaller cities like Gwalior present opportunities for long-term investment at low entry costs.

Each city has its unique advantages, and buyers should consider factors such as employment opportunities, infrastructure, and lifestyle preferences before making a decision.

In conclusion, avoiding the property dealer trap in India requires a combination of awareness, planning, and strategic decision-making. Whether through collective construction or smart purchasing, buyers can significantly reduce costs and gain greater control over their investments. By leveraging legal frameworks, financial tools, and market insights, it is possible to turn the dream of homeownership into a practical and affordable reality.