India always imported far more goods than it exported, particularly crude oil. Since international oil trade is largely denominated in US dollars, India constantly needed dollars to pay for energy imports. This created steady downward pressure on the rupee. Even when exports grew, imports often grew faster

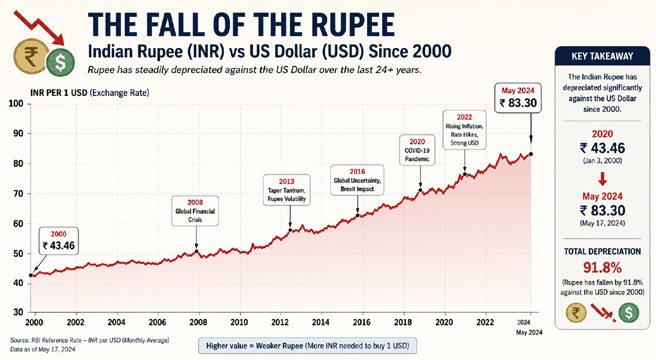

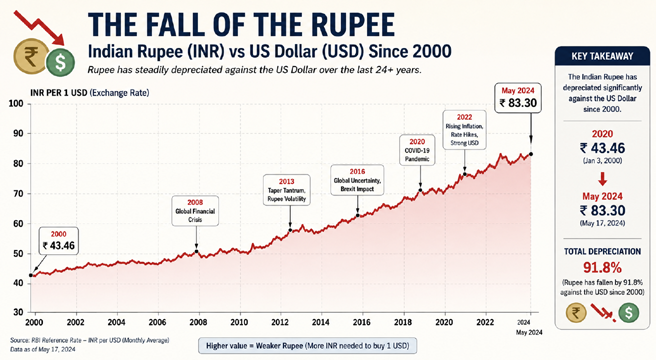

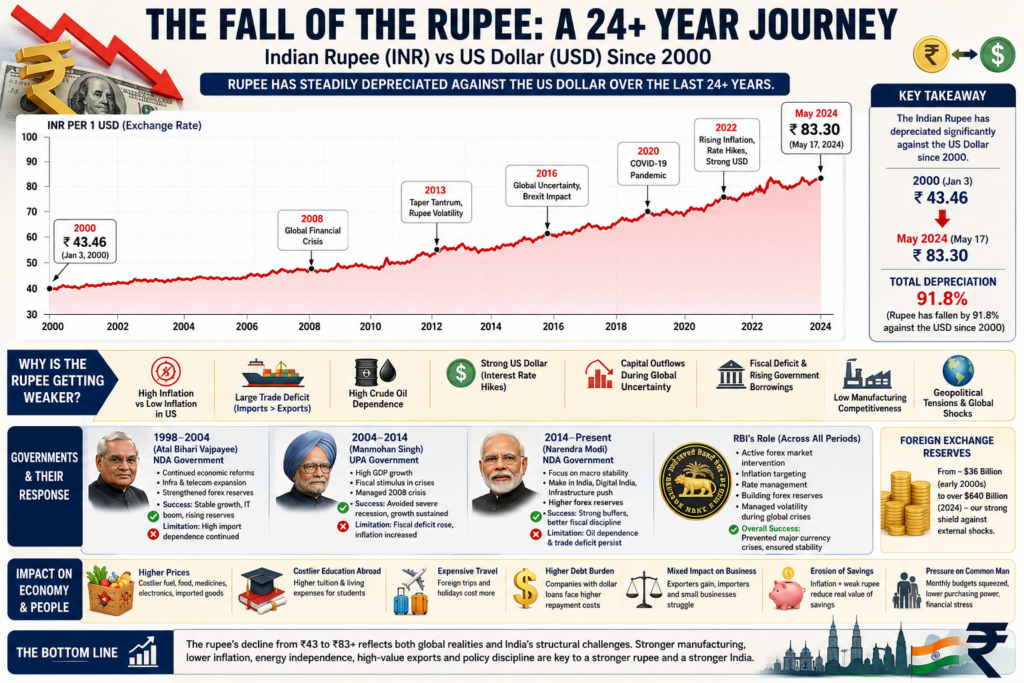

The story of the Indian rupee’s decline against the United States dollar since 2000 is not merely a story about exchange rates. It is the story of India’s changing place in the global economy, the pressures of oil imports, widening trade deficits, inflation, global crises, domestic policy decisions and the everyday struggles of ordinary Indians trying to preserve purchasing power in a rapidly changing world. Over the past two-and-a-half decades, the rupee has steadily weakened from around ₹43.46 per US dollar in early 2000 to over ₹83 per dollar by 2024. This depreciation has happened gradually, interrupted occasionally by sharp crises, speculative attacks, geopolitical shocks and global financial disruptions.

The infographic tracking the rupee’s decline since 2000 captures not just a currency movement but the broader economic anxieties of a developing nation deeply integrated into global trade and finance. The graph reveals how the rupee moved through successive phases of stress: the aftermath of India’s economic liberalisation, the 2008 global financial crisis, the 2013 taper tantrum, Brexit-era global uncertainty, the COVID-19 pandemic and the post-pandemic inflationary cycle that strengthened the US dollar worldwide.

At the start of the millennium, India was under the leadership of the National Democratic Alliance government headed by Atal Bihari Vajpayee. India’s economy was still emerging from the structural reforms initiated in 1991. Foreign exchange reserves were improving compared to the crisis years of the early 1990s, but India remained heavily dependent on imports for crude oil, defence equipment and advanced industrial machinery. The rupee hovered around ₹43 to ₹45 per dollar during this period.

The Vajpayee government pursued infrastructure expansion, telecom liberalisation and disinvestment policies that helped accelerate economic growth. The IT and software services boom also strengthened India’s foreign exchange earnings. Companies like Infosys, TCS and Wipro expanded globally, bringing in valuable dollar revenues. Yet even during these relatively stable years, the rupee showed a gradual tendency toward depreciation. One major reason was inflation differentials. India historically recorded higher inflation than the United States. When inflation remains persistently higher in one country, its currency gradually loses purchasing power relative to currencies of lower-inflation economies.

Another structural issue was India’s persistent trade deficit. India imported far more goods than it exported, particularly crude oil. Since international oil trade is largely denominated in US dollars, India constantly needed dollars to pay for energy imports. This created steady downward pressure on the rupee. Even when exports grew, imports often grew faster.

The period between 2004 and 2008 under the United Progressive Alliance government headed by Manmohan Singh initially appeared economically strong. India experienced high GDP growth rates exceeding 8 percent annually in several years. Foreign institutional investors poured money into Indian equity markets. Global investors viewed India as a rising economic power. For a brief period in 2007, the rupee even appreciated toward ₹39 per dollar as capital inflows surged.

However, beneath the optimism lay vulnerabilities. Rapid economic expansion increased demand for imports. Oil prices surged globally, touching nearly $147 per barrel in 2008. India’s current account deficit widened sharply. Then came the global financial crisis of 2008 following the collapse of Lehman Brothers in the United States. International investors rushed toward safe-haven assets such as the US dollar and US Treasury bonds. Capital fled emerging markets including India.

The rupee weakened rapidly, moving beyond ₹50 per dollar. The UPA government and the Reserve Bank of India responded with liquidity injections, fiscal stimulus measures and monetary easing to prevent economic collapse. Public spending increased significantly to maintain growth and protect employment. While India avoided the catastrophic banking failures seen in Western economies, the fiscal deficit widened substantially.

The government’s response succeeded in preventing a severe recession, but it also laid foundations for later inflationary pressures. Excessive fiscal expansion combined with supply-side bottlenecks contributed to rising food inflation and weakening macroeconomic fundamentals in the following years. Inflation eroded household savings and increased the cost of living for ordinary Indians.

For common citizens, the weakening rupee had immediate and visible effects. Imported goods became more expensive. Petroleum prices rose. Since fuel costs influence transportation expenses, almost every product in the economy became costlier over time, vegetables, milk, cooking gas, medicines, electronics and consumer goods. Families found their monthly budgets under increasing stress. Middle-class aspirations such as foreign education, overseas travel and imported cars became significantly more expensive.

The depreciation also affected Indian students studying abroad. Tuition fees and living expenses denominated in dollars became far costlier when converted into rupees. Families often had to borrow more or liquidate assets to finance overseas education. Similarly, businesses dependent on imported machinery or raw materials faced rising operational costs.

Yet a weaker rupee was not entirely negative. Indian exporters benefited because their goods and services became cheaper in global markets. The IT services industry especially gained because software companies earned revenues in dollars while paying salaries in rupees. Business process outsourcing, pharmaceuticals and textile exporters also benefited to varying degrees. This created an important paradox in India’s exchange rate debate: a weaker rupee hurt consumers and importers but helped exporters.

Crisis after crisis: taper tantrums, global uncertainty and India’s balancing act

The years after the global financial crisis exposed the deeper fragility of India’s external sector. By 2012 and 2013, India faced one of the most severe currency pressures in recent decades. The rupee collapsed toward ₹68 per dollar during what became known globally as the “taper tantrum.”

The crisis began when the US Federal Reserve signaled that it might gradually reduce its quantitative easing programme initiated after the 2008 crisis. Investors feared rising US interest rates and began withdrawing money from emerging markets. Countries with large current account deficits such as India, Brazil, Turkey and South Africa were especially vulnerable. India was grouped among the so-called “Fragile Five” economies.

Under Prime Minister Manmohan Singh and Finance Minister P. Chidambaram, the government implemented emergency measures to stabilise the rupee. Gold imports were restricted because India’s massive appetite for gold was worsening the trade deficit. The RBI raised short-term interest rates to discourage currency speculation and attract capital inflows. Special swap windows were opened for oil companies and banks to ease dollar demand pressures.

The appointment of Raghuram Rajan as RBI Governor in 2013 helped restore investor confidence. Rajan introduced measures to attract foreign currency deposits from non-resident Indians and stabilize capital flows. Over time, these policies succeeded in calming markets, and the rupee recovered partially.

However, the episode exposed India’s structural dependence on foreign capital and imported energy. Whenever global investors become risk-averse, the rupee tends to weaken sharply because India requires continuous foreign capital inflows to finance its deficits.

In 2014, the National Democratic Alliance returned to power under Prime Minister Narendra Modi. The new government focused heavily on macroeconomic stability, infrastructure expansion, manufacturing initiatives and digitalisation. Campaigns such as “Make in India” aimed to reduce import dependence and boost domestic manufacturing.

The Modi government inherited both opportunities and vulnerabilities. On one hand, global oil prices collapsed dramatically after 2014, giving India temporary relief because crude imports became cheaper. On the other hand, global uncertainties persisted. The Brexit referendum in 2016, geopolitical tensions and fluctuating capital flows continued exerting pressure on emerging market currencies.

The government and RBI adopted inflation targeting frameworks to stabilize prices. Fiscal discipline improved compared to earlier years. Foreign exchange reserves rose substantially, giving India stronger buffers against external shocks. Yet despite these improvements, the rupee continued its long-term depreciation trend.

One reason was the relentless strength of the US dollar itself. The dollar remains the world’s dominant reserve currency. During periods of uncertainty, global investors flock to dollar-denominated assets. Emerging market currencies therefore face structural disadvantages. India’s relatively higher inflation compared to advanced economies also continued eroding the rupee’s value gradually.

Another reason was India’s manufacturing weakness. Despite initiatives like Make in India, India remained heavily dependent on imports for electronics, semiconductors, solar equipment, crude oil and industrial machinery. India’s consumer demand expanded rapidly, but domestic manufacturing often failed to keep pace. This widened trade imbalances.

The demonetisation decision of 2016 created additional economic disruption, although its direct impact on the exchange rate was mixed. Economic growth slowed temporarily as cash-dependent sectors suffered severe liquidity shortages. Informal businesses, small traders and daily wage workers faced enormous hardships. While digitisation increased, the broader economy experienced stress that indirectly affected investor confidence and growth momentum.

The introduction of the Goods and Services Tax (GST) in 2017 aimed to unify India’s fragmented tax system and improve efficiency. Over the long term, GST strengthened formalisation and tax compliance. However, its implementation initially created disruptions for small businesses and supply chains.

For ordinary Indians, the weakening rupee increasingly translated into inflationary pressure. Fuel price hikes affected transportation and electricity costs. Cooking gas cylinders became more expensive. Imported edible oils, electronic gadgets, smartphones and medical equipment cost more. Airline tickets and foreign holidays became significantly pricier. Inflation particularly hurt lower-income households because a larger share of their income went toward essentials such as food and transport.

Urban middle classes also felt the squeeze. Even salaried professionals earning more than previous generations found their purchasing power eroding due to rising housing costs, education expenses and imported inflation. Savings parked in low-interest bank deposits often failed to keep pace with inflation and currency depreciation.

Meanwhile, Indian companies with dollar-denominated debt faced growing repayment burdens whenever the rupee weakened. Infrastructure firms, airlines and telecom companies with foreign loans experienced increased financial stress. Currency depreciation effectively raised their debt obligations in rupee terms.

Despite these problems, India’s growing foreign exchange reserves became a critical defense mechanism. The RBI intervened periodically in currency markets by selling dollars to prevent excessive rupee volatility. By accumulating reserves exceeding hundreds of billions of dollars, India strengthened its ability to withstand external shocks compared to the fragile conditions of the early 1990s.

Pandemic shock, inflation wars and the burden on common citizens

The COVID-19 pandemic marked another historic turning point for the rupee and the global economy. When the pandemic erupted in 2020, financial markets worldwide entered panic mode. Investors rushed toward safe-haven assets, especially the US dollar. Emerging market currencies weakened sharply, including the Indian rupee.

Under Prime Minister Narendra Modi and RBI Governor Shaktikanta Das, India implemented a mix of fiscal support, monetary easing and liquidity measures to prevent economic collapse. The RBI slashed interest rates, infused liquidity into banks and introduced loan moratoriums. The government announced relief packages under the Atmanirbhar Bharat initiative.

These measures helped prevent a systemic financial meltdown, but the economic pain was immense. Lockdowns devastated informal workers, migrant labourers, small traders and service industries. GDP contracted sharply in 2020. Tax revenues fell while public spending rose dramatically.

The rupee weakened again as economic uncertainty surged. However, India’s large foreign exchange reserves prevented a full-blown currency crisis. Unlike the 1991 balance-of-payments emergency, India possessed substantial reserve buffers that reassured investors.

The post-pandemic world introduced a new challenge: global inflation. Massive stimulus programmes worldwide combined with supply chain disruptions pushed prices higher across countries. Then came the Russia-Ukraine war in 2022, which triggered a surge in global crude oil, gas and food prices.

The US Federal Reserve responded aggressively by raising interest rates. Higher US interest rates strengthened the dollar globally because investors could earn better returns on dollar assets. As capital moved back toward the United States, emerging market currencies weakened again.

The rupee crossed ₹80 per dollar and moved toward ₹83 by 2024. The RBI intervened heavily to slow the pace of depreciation. India’s foreign exchange reserves were used strategically to prevent panic and excessive volatility. The government also attempted to diversify energy imports and negotiate discounted crude purchases from Russia to manage oil costs.

Yet the underlying structural pressures remained. India still imported the majority of its crude oil requirements. Every rise in global oil prices widened the current account deficit and increased demand for dollars. Electronics imports also surged because of India’s rapidly growing digital economy.

The weakening rupee had profound consequences for daily life. Fuel inflation became one of the biggest burdens on households. Transportation costs increased across sectors. Food inflation intensified because agricultural transportation and fertilizer costs rose. Cooking oil prices surged due to import dependence. Urban commuters paid more for petrol and diesel, while rural households faced higher costs for agricultural inputs.

Medical inflation also became a major concern. India imports substantial amounts of medical devices, advanced pharmaceutical ingredients and diagnostic equipment. A weaker rupee increased healthcare costs over time. Families already burdened by private medical expenses found themselves under growing financial stress.

Education abroad became dramatically costlier. A student paying $50,000 annually in tuition would have needed roughly ₹21 lakh in 2000 terms but over ₹41 lakh at exchange rates above ₹83 per dollar, excluding inflation in foreign universities themselves. This placed enormous pressure on middle-class families aspiring for global education.

Travel and tourism costs also soared. Foreign vacations became luxury expenditures for many Indians. International hotel bookings, airline tickets and shopping abroad became substantially more expensive in rupee terms.

At the same time, exporters continued benefiting from a weaker rupee. IT giants, pharmaceutical companies and software exporters earned larger rupee revenues from dollar earnings. Remittances sent home by Indians working abroad also became more valuable in rupee terms, benefiting many families.

However, relying excessively on currency depreciation to boost exports carries risks. Sustainable export competitiveness ultimately depends on productivity, innovation, infrastructure and manufacturing capability rather than merely exchange rate weakness.

One of the biggest long-term concerns is imported inflation. Since India imports energy, electronics and industrial inputs extensively, currency weakness transmits global inflation directly into the domestic economy. Persistent inflation reduces real wages and weakens household savings.

The psychological dimension of rupee depreciation is equally important. A steadily weakening currency affects national confidence and perceptions of economic strength. Many Indians compare the rupee’s trajectory against the dollar and conclude that the economy is underperforming, even though exchange rates alone do not fully measure economic health.

Still, the trend raises legitimate concerns about structural weaknesses. India’s manufacturing share remains lower than many East Asian economies. Export diversification is limited compared to countries like China. Energy dependence remains extremely high. Domestic inflation often exceeds that of advanced economies. Fiscal deficits remain elevated. All these factors contribute to long-term currency pressure.

Successive governments have attempted various solutions. The Vajpayee government accelerated liberalisation and infrastructure growth. The Manmohan Singh government pursued high-growth expansion and crisis stabilization after 2008. The Modi government emphasized macroeconomic discipline, digitisation, manufacturing promotion and reserve accumulation. Each government achieved partial successes while also confronting structural constraints beyond immediate political control.

The RBI has perhaps played the most consistently stabilising role across administrations. By actively managing foreign exchange reserves, controlling inflation expectations and intervening during crises, the central bank prevented severe currency collapses even during periods of global turmoil.

The future trajectory of the rupee will depend on several critical factors: reducing oil dependence through renewable energy expansion, strengthening manufacturing competitiveness, increasing high-value exports, controlling inflation and maintaining investor confidence. India’s growing digital economy, startup ecosystem and infrastructure investments offer long-term opportunities, but structural reforms remain essential.

The rupee’s decline from ₹43 to beyond ₹83 over two decades reflects both global economic realities and India’s internal vulnerabilities. It tells the story of a nation rising economically yet still struggling with import dependence, inflation and external shocks. For ordinary Indians, the weakening rupee has meant higher living costs, shrinking purchasing power and growing economic anxiety. For policymakers, it remains a continuous balancing act between growth, inflation control, export competitiveness and financial stability.

The rupee’s journey ultimately reminds India of an uncomfortable truth: economic strength is not measured only by GDP growth headlines or stock market rallies. It is also measured by the stability of purchasing power, the resilience of domestic industry, the strength of exports and the ability of ordinary citizens to maintain dignity and prosperity in everyday life.